Finch & Beak is now SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

We invite you to check out the SLR website, so you can see the full potential of what we offer, from sustainability strategies to implementation covering Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, Responsible Sourcing and more.

Publ. date 22 Mar 2023

Publ. date 22 Mar 2023When it comes to incorporating ESG considerations into their businesses, companies can approach the double materiality assessment by meeting the requirements set out by regulations, which is essential to operate within the law and maintain their social license to operate. However, meeting regulatory requirements alone may not fully capture the potential benefits of ESG considerations. On the other hand, taking a strategic approach to the double materiality assessment process can help companies identify opportunities to improve their sustainability performance, mitigate risks, and build stronger relationships with stakeholders.

It is important to note that compliance and strategic benefits are not mutually exclusive. Companies can meet regulatory requirements while also using the double materiality assessment process to gain strategic benefits. One way to do this is by considering the long-term implications of their ESG impacts, both positive and negative, and how they align with the organization's values and strategic goals.

By taking a strategic approach to their double materiality assessment, a company like Ørsted has identified opportunities to invest in sustainable practices that not only reduce negative environmental impacts but also improve operational efficiency and lower costs over time. This has allowed them to make progress toward their sustainability goals while also benefiting their bottom line. The company has set ambitious sustainability goals, including achieving carbon neutrality in its operations and energy generation by 2025 and reducing the carbon footprint of its energy products by 50% by 2030. To achieve these goals, Ørsted has invested heavily in offshore wind technology and has transitioned away from coal-based energy production. In addition, the company has implemented a number of sustainability initiatives, such as reducing waste and water usage in their operations and promoting sustainable transportation among their employees.

Interested in hearing more about leveraging your double materiality assessment? Sign up for the webinar on Thursday 13th of April 2023, 15-16h CET. |

As already proposed in the article Double Materiality: 3 Tips for a Practical Approach, in order to implement a double materiality approach in line with CSRD, organizations should start with the impact perspective, take a global and a 'local' approach, and take a forward-looking perspective. To conduct an exercise that incorporates a strategic lens into the process, our methodology proposes a novel approach for some of the key elements of the double materiality assessment:

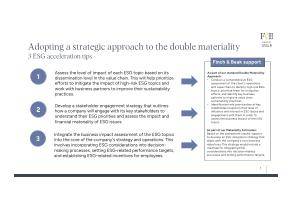

a. Value Chain Analysis: Organizations are required to assess the material impacts, risks, and opportunities associated with their direct and indirect business relationships in the upstream and/or downstream value chain. It is relevant for an organization to map the areas where ESG topics are likely to arise based on the nature of the organization's activities and business relationships and identify those topics that are spread and mappable across the whole value chain.

The level of impact of each topic can then be assessed by taking into account its dissemination level in the organization's value chain: ESG topics that have a high level of dissemination throughout the value chain are likely to have a higher overall impact, while topics with lower dissemination levels may have a lower overall impact. Through mapping its upstream and downstream relationships, a global telecommunication player may identify for example risks related to the sourcing of conflict minerals, which can lead to negative impacts on local communities and the environment. By considering the level of impact of this topic according to its dissemination level in the value chain, the organization can prioritize efforts to source conflict-free minerals and work with suppliers to improve their sustainability practices. This can ultimately help the organization mitigate reputational risks and build stronger relationships with stakeholders, including customers and investors, who increasingly prioritize ethical and sustainable practices.

In our latest article discussing the changes to the CSA 2023 methodology, we highlighted the increased focus on supply chain management as a critical component of investors' expectations. The new methodology emphasizes the importance of responsible sourcing, transparency, and traceability throughout the value chain, which can help investors and companies identify and mitigate ESG risks and opportunities. By taking supply chain management into account, organizations can build stronger relationships with stakeholders, meet the growing demand for socially and environmentally responsible products, and gain a competitive advantage in the market.

b. Business Impact Assessment: Assessing the impact of sustainability topics is a complex process that requires careful consideration of several factors. There are two main types of assessment to consider: impact materiality and financial materiality. Both types of materiality should be analyzed carefully and used to inform decisions on how to reduce negative impacts or increase positive ones:

- Impact Materiality: refers to the scale, scope, and irremediable character of an ESG topic's impact. Scale indicates the gravity of the impact, such as its effects on human health, the environment, or society. Scope indicates the geographic extent of the impact. For example, if a sustainability topic's impact is focused on a specific region, then actions should be developed for the specific sites concerned rather than at group level. The irremediable character indicates the extent to which the negative impact can be remediated, and the urgency to develop a preventive approach to the impact is higher when the irremediability is low.

- Financial materiality: refers to the size and likelihood of an ESG topic’s impact. Size indicates the amount of financial impact a sustainability topic could have on an organization, while likelihood refers to the probability of the impact occurring.

To illustrate, let's take the example of a manufacturing organization that produces a significant amount of GHG emissions. GHG emissions are widely recognized as contributing to climate change, which can have significant environmental and societal impacts on a global scale. While the impact of this particular organization's emissions may vary depending on factors such as its industry, location, and regulatory environment, it is reasonable to assume that the potential impact on society and the environment could be significant in terms of its contribution to climate change. The irremediable character of the impact is high, as it is difficult with the currently available technologies to reverse the damage already done. Therefore, the urgency to develop a preventive approach to reduce emissions is high.

In terms of financial materiality, the size of the impact could be significant if the organization incurs fines for non-compliance with emissions regulations or if it incurs costs to reduce emissions. The likelihood of the impact is also high, given the increasing regulatory pressure to reduce emissions and growing stakeholder concerns about climate change. To reduce its negative impact, the manufacturing organization could implement several actions, such as investing in renewable energy sources, improving energy efficiency, or shifting to low-carbon production processes. By taking a proactive approach to sustainability topics, companies can not only reduce their negative impact but also create new opportunities for business growth and innovation.

c. Stakeholder Engagement: It is important that an organization engages with its key stakeholders, not only to understand its ESG priorities but also to assess the impact and financial materiality. Although not all stakeholders have detailed knowledge about the organization's business, some stakeholders have deeper knowledge about aspects of specific phases of the value chain and could provide useful insights into the indirect impacts of (and on) an organization. This activity should also be carried out with the aim of mapping opportunities for collaboration and engagement with different stakeholders, so a positive value can be created inside and outside the organization and negative impacts can be reduced.

The engagement process could reveal that an organization’s employees are interested in more sustainable workplace practices, such as reducing waste and increasing recycling. This is particularly important for Microsoft, as waste reduction is part of the identified material topics for the company, specifically under Natural Resources. Through its Zero Waste Microsoft implemented a comprehensive waste management program and encouraged its employees to participate in it, leading to a reduction in the organization's environmental impact and the creation of a more sustainable work culture. By prioritizing waste reduction as part of its double materiality assessment, Microsoft was able to align its sustainability goals with the values and concerns of its employees, resulting in a successful and impactful initiative.

The double materiality assessment process is not only essential for complying with ESG regulations but also offers strategic benefits for companies. By adopting a strategic approach to the double materiality assessment process, companies can identify opportunities to enhance their sustainability performance, strengthen stakeholder relationships, and ultimately drive business growth. To address this challenge, here are three actionable ESG acceleration tips:

If you would like to know more about double materiality or require assistance with your double materiality assessment, contact us

Photo by J. Schiemann on Unsplash

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.