Thank you for visiting the Finch & Beak website. Finch & Beak is now part of SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

This is an exciting time for us, as our team now includes an array of new colleagues who offer advisory and technical skills that are complementary to our own including Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, and Responsible Sourcing.

We would like to take this opportunity to invite you to check out the SLR website, so you can see the full potential of what we are now able to offer.

Publ. date 19 Jun 2023

Publ. date 19 Jun 2023The ESRS is a set of 12 standards desired by European Commission to improve the availability of credible and comparable ESG data, thus reducing the reporting burden for organizations.

CSRD understands and promotes the international relevance of the GRI standards that is why the EU has decided to develop the ESRS in alignment with them, meaning that organizations that already use those standards will be better prepared to comply with ESRS requirements. On top of that, ensuring alignment between the ESRS and GRI will help achieve global comparability - enhancing quality and usability - and limit duplicated reporting requirements.

Despite the similitudes, there will also be differences between GRI’s impact-focused global standards and the double-materiality-focused EU standards as prescribed by the CSRD.

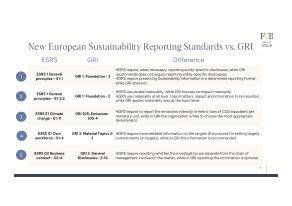

The attached download includes a comprehensive table that provides in-depth information and highlights the key differences between ESRS and GRI.

Besides those novelties brought by the new reporting standards, there are also some similarities, in fact, as explained by GRI, the ESRS Standards are, as much as possible, fully aligned with the GRI Standards. Essentially, they share the goal of creating a comprehensive reporting system which enhance the transparency and the dialogue between companies and their stakeholders.

Even if the topics and the requirements in the ESRS will be expanded over time, the two different standards overlap in content and strict reporting requirements. For instance, the ESRS structure closely resembles that of the GRI, consisting of four main areas:

The cross-cutting standards create a basis for all content of the topic-specific standards, therefore defining the fundamental concepts of the disclosure requirements.

Within the 4 areas that are composed by the 12 standards in total, corresponding disclosure requirements are specified with similarities to the GRI, like for “ESRS E1-6” regarding the total and the different GHG emissions. On the contrary, for instance, the ESRS require Scope 3 disclosure regardless of materiality.

Despite the similarities between GRI and ESRS, the latter provides disclosure novelties, for example, reducing flexibility in the way data should be presented, and in addition, a more comprehensive ESG data collection following the double materiality principle.

In addition, the ESRS will be legally binding for certain organizations - startingfrom 2024 - representing a decisive advantage for the availability and comparability of data compared to GRI.

Given their gradual introduction, it may be possible that in near future the ESRS will surpass the GRI in the EU in terms of application, becoming a fundamental part for the systematic reporting routine for all kind of companies.

Overall, the adoption of ESRS guidelines and therefore the double materiality framework has the potential to accelerate an organization’s sustainability strategy through deep understanding of outside-in and inside-out ESG impacts. The results of the process unveil both ESG risks and opportunities for the company, and those results must be signed off by the board. This is not only a game-changer but also and more importantly a chance to onboard the leadership and position ESG at the heart of the company’s strategy.

If you are looking for personal guidance in the assessment process, please contact Johana Schlotter at Johana@finchandbeak.com or call +31 6 28 02 18 80 to discuss how Finch & Beak can help you improve your ESG performance.

Photo by Cole Keister on Unsplash

Positive thinker with passion and involvement in sustainability and climate change, trying to find suitable solutions for everyday business activities. | gabriele@finchandbeak.com

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.