Thank you for visiting the Finch & Beak website. Finch & Beak is now part of SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

This is an exciting time for us, as our team now includes an array of new colleagues who offer advisory and technical skills that are complementary to our own including Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, and Responsible Sourcing.

We would like to take this opportunity to invite you to check out the SLR website, so you can see the full potential of what we are now able to offer.

Publ. date 20 Jul 2023

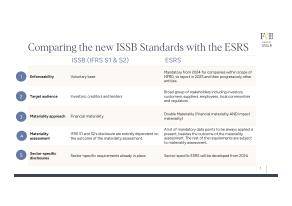

Publ. date 20 Jul 2023In June 2023, the International Sustainability Standards Board (ISSB) published new reporting standards enabling a new era of sustainability-related disclosures in capital markets worldwide. These standards, namely IFRS S1 and IFRS S2, were issued to harmonize the reporting standards at global level and to meet investors’ demands for consistent and comparable sustainability disclosures.

More specifically, IFRS S1 provides a set of disclosure requirements designed to enable companies to communicate to investors about sustainability-related risks and opportunities they face over the short, medium and long term. IFRS S2, on the other hand, sets out specific climate-related disclosures. Both fully incorporate the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD).

Similarly, the ESRS - European Sustainability Reporting Standards – was adopted in July in order to enhance the credibility and comparability of ESG data among the EU companies.

With this new panorama of reporting standards, it is important to discover the unique characteristics that both standards will introduce.

In the attached download of this article, a comprehensive table is included that provides detailed information and highlights of the key distinctions between ISSB and ESRS.

Despite their differences, both sets of standards use the TCFD framework structure. Moreover, the connection and interaction with the GRI standards is well present in both standards. They also align on some key concepts like value chain information requirements.

The decision between applying one set of standards or another might be difficult especially because a full interoperability between ISSB and ESRS standards seems unlikely. In fact, as seen before, they differ a lot especially when looking at the inclusiveness of the stakeholders, the enforceability and the approach to the Materiality analysis.

Even if sometimes organizations are forced to follow ESRS requirements due to the size or the location of the business, the elements specific to ESRS previously described - such as the number of stakeholders involved or the approach used for the assessment of material topics - go further than those of ISSB and therefore can help better understand the company’s impact and therefore shape the ESG performance of the company.

In this regard, the Double-materiality analysis approach goes beyond simple reporting. It is a crucial tool to identify opportunities and leverage organizations’ sustainability strategies while strengthening stakeholder relationships, mitigating risks and ultimately leading business growth. Indeed, a good interpretation of the results of the double materiality assessment helps companies also work on their outreach to various groups of stakeholders, their reputation and talent attraction potential.

Finally, ISSB standards provide more freedom regarding the location of information disclosures whereas the CSRD – therefore ESRS – prescribes a specific structure within companies’ management reports.

To conclude, the recently introduced ESRS seem to be more practical and beneficial from a company’s strategic point of view, in comparison with the ISSB standards. In fact, due to its reporting structure, the double-materiality approach and the involvement of a broader group of stakeholders, ESRS can be used as an opportunity to go beyond reporting and accelerate your sustainability strategy.

If you are looking for personal guidance about the double-materiality assessment process, please contact Johana Schlotter at Johana@finchandbeak.com or call +31 6 28 02 18 80 to discuss how Finch & Beak can help you improve your ESG performance.

Photo by Edho Fitrah on Unsplash

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.