Thank you for visiting the Finch & Beak website. Finch & Beak is now part of SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

This is an exciting time for us, as our team now includes an array of new colleagues who offer advisory and technical skills that are complementary to our own including Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, and Responsible Sourcing.

We would like to take this opportunity to invite you to check out the SLR website, so you can see the full potential of what we are now able to offer.

Publ. date 9 Oct 2023

Publ. date 9 Oct 2023The S&P Global Corporate Sustainability Assessment (CSA) is an ESG rating tool that helps companies identify and disclose their sustainability risks and performance covering a wide range of sustainability topics. It provides participating companies with a score that reflects their ESG performance, which can be used by investors, customers, and other stakeholders to make informed decisions. and identifying areas of improvement.

Exploring how the CSA can serve as a compass for companies navigating the complexities of CSRD compliance, this article provides insights on the alignment between the CSA's comprehensive sustainability coverage and the CSRD's mandated disclosure themes.

The CSA offers a wide range of sustainability topics, many of which overlap with the requirements of the CSRD. This overlap can assist companies in identifying the sustainability topics needed for disclosure, collecting and analysing sustainability-related information, developing ESG targets and metrics, and receiving valuable feedback on their sustainability performance, ultimately supporting enhanced environmental, social, and governance stewardship within the forthcoming regulatory landscape.

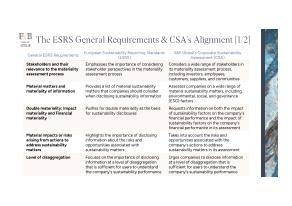

While ESG metrics are vast and vary by industry, company size, company location and complexity, there are still synergies across the sustainability topics. The S&P Global CSA covers the main disclosure themes for the CSRD, including:

To learn more about how the CSA aligns with the General Requirements of the European Sustainability Reporting Standards (ESRS) issued by the CSRD, download our analysis in the attached.

The questions and criteria in the CSA are aligned with the CSRD's requirements across its disclosure themes. This can help companies to identify the sustainability issues that are most material to their business and to start collecting data on their performance in these areas. While the CSA preselects the material issues based on industry, the CSRD is industry-agnostic and the material issues are based on what is deemed material through conducting the double materiality assessment.

It is good to keep in mind that the effort put in closing the gaps when participating in the CSA may yield gains in CSRD preparedness. Practicing through responding to the CSA can help companies practice data collection with the provision of a score that can inform companies on how well they are performing and disclosing prior to the CSRD coming into effect as of 2025. By participating in the CSA, companies can gain the knowledge and insights they need to comply with the CSRD and to communicate their sustainability performance effectively, and start proactively preparing for CSRD compliance.

While the CSA provides a roadmap for CSRD readiness, it is not a comprehensive tool to prepare for disclosure in accordance with the directive. Want to ensure that you are CSRD ready? In just 5 days, Finch & Beak could provide you with full visibility of your CSRD gaps. Finch & Beak could help you understand and prepare for the CSRD, future-proof your company for upcoming regulations and fast-track your CSRD alignment.

Finch & Beak enables companies across various sectors to gain a deep understanding of S&P Global’s CSA, its structure, relevance, and how to unlock the full potential of their participation in the assessment. Along with our benchmarking tools across ESG rating systems such as the ESG Streamliner, we have prepared an acceleration checklist for CSA activation, to help drive your company’s sustainability performance. To know more, and to further discuss how to make the most of the array of benchmarks to mobilize your sustainability action, please contact Johana Schlotter at Johana@finchandbeak.com or call +31 6 28 02 18 80.

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.