Finch & Beak is now SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

We invite you to check out the SLR website, so you can see the full potential of what we offer, from sustainability strategies to implementation covering Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, Responsible Sourcing and more.

Publ. date 9 Oct 2023

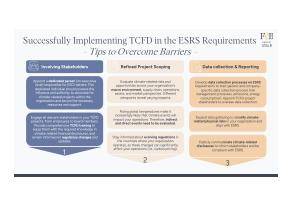

Publ. date 9 Oct 2023Download our guide for actionable tips to overcome common implementation barriers and enhance your organization's transparency and sustainability reporting.

In today's business landscape, sustainability must be a core component of corporate strategy. In response to an emerging landscape of increasing stakeholder requirements on ESG, the European Union introduced Corporate Sustainability Reporting Directive (CSRD), which is translated into ESRS to increase sustainability disclosures by companies.

In 2017, the Task Force on Climate-related Financial Disclosures (TCFD) framework was created to guide organizations in transparently and consistently presenting climate-related financial risks and opportunities. These aspects have now been incorporated into ESRS.

Importantly, ESRS has adopted all 11 recommended disclosures from the TCFD framework. When comparing TCFD to ESRS, ESRS includes disclosure requirements from "ESRS 2 General Disclosures" and "ESRS E1 Climate Change", broadening its focus beyond just climate-related issues. Therefore, ESRS enhances the initial TCFD requirements by introducing additional elements that offer a more comprehensive view of a company's sustainability endeavors.

Both standards share similarities when it comes to Governance guidance, asking for a clear climate governance structure, including board oversight, to manage and address climate-related risks and opportunities. Nonetheless, ESRS asks whether remuneration is tied to GHG emission reduction targets under Governance, whereas TCFD lists it under Metrics & Targets.

On the Strategy element, both TCFD and ESRS require companies to use climate-related scenario analysis as a tool for developing a climate strategy and building resilience against climate-related risks. However, ESRS goes a step further by delving deeper into the effects of climate-related risks on future financial position and business activities, distinguishing between physical and transition risks. Notably, ESRS E1 also outlines more explicit targets and disallows the use of carbon credits/offsets to achieve GHG emission reduction targets, while incorporating elements of the EU Taxonomy Regulation.

On Risk Management, both frameworks ask how the organization manages and mitigates climate-related risks, integrating them into broader risk management practices. ESRS however also intertwines the concept of double materiality, in which climate-related risks and opportunities play a role.

Food company Danone, which has started already its TCFD journey, has conducted a thorough assessment of climate-related transitional and physical risks and highlights the significance of the potential financial impact. The company has translated the risk and opportunity findings into policies and action plans, integrating them with the company’s strategy. Moreover, the company also started their journey on reporting on EU Taxonomy and therefore sets an important milestone for ESRS.

Finally, on Metrics & Targets level, companies are asked to disclose on climate-related performance metrics and targets, along with progress toward achieving those targets, to assess the organization's climate-related impacts and efforts. ESRS goes a step further in terms of reporting requirements. For instance, while TCFD asks also for disclosing Scope 1-3 emissions and the targets behind, ESRS requires the distinction of three levels of targets: general climate-related targets, GHG emission reduction targets, and net zero targets. Also, here EU Taxonomy elements are added, like the turnover, CapEx, OpEx.

Digital automation and energy management company Schneider Electric discloses on TCFD elements and has already defined and started to implement programs or activities to achieve the emission reduction targets of Scopes 1-3, which is also an important milestone of both TCFD and ESRS.

Organizations that have proactively started to integrate TCFD requirements in their reporting have a head start, as they only need to add the supplementary components stemming from ESRS, while those that have not initiated this process will have to begin from scratch to meet ESRS demands. Both reporting frameworks require the disclosure of various climate-related elements, but the key emphasis is on integrating these processes within the organization to effectively manage climate risks, capitalize on opportunities, and prepare for a resilient and sustainable future.

To assess your company's preparedness, one of the initial steps outlined in Finch & Beak's 6-phase TCFD roadmap is to identify TCFD, including ESRS reporting disclosure gaps. Subsequently, as you navigate through the various phases, including phases Risk and opportunity analysis, Scenario Analysis and integrating climate scenarios into strategy and targets, the last step is disclosing climate-related findings in accordance with ESRS. This comprehensive approach ensures that your organization thrives in an era where sustainability and transparency are paramount.

At Finch & Beak, our purpose is to accelerate sustainability within the business of our clients. Together with our fellow companies from SLR Consulting, we offer a wide range of TCFD support services:

If your organization requires support on integrating the TCFD framework or strengthening your climate strategy contact us at hello@finchandbeak.com or +34 627 788 170 to discuss how Finch & Beak can assist you.

¹ Task Force on Climate-related Financial Disclosures (2022): 2022 Status Report

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.