Finch & Beak is now SLR Consulting, a global organization that supports its clients on setting sustainability strategies and seeing them through to implementation.

We invite you to check out the SLR website, so you can see the full potential of what we offer, from sustainability strategies to implementation covering Climate Resilience & Net Zero, Natural Capital & Biodiversity, Social & Community Impact, Responsible Sourcing and more.

Publ. date 1 Feb 2024

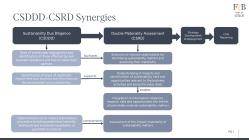

Publ. date 1 Feb 2024The European Corporate Sustainability Due Diligence Directive (CSDDD) and the Corporate Sustainability Reporting Directive (CSRD) are both part of the European Commission’s efforts to increase transparency and traceability of the harmful impacts and consequences of corporate operations and their value chains. Although their scope and timeline for coming into force differ, these two EU directives are meant to work together and be applied in parallel by corporate entities: the first (CSDDD) as a framework for what due diligence obligations corporations in scope will bear, and the second (CSRD) as a framework for how companies should report on these obligations.

One of the main synergies between the two directives is the strong linkage between the double materiality assessment to be conducted by companies in scope of the CSRD and the sustainability due diligence process to be implemented by companies in scope of the CSDDD. Other synergies are related to 1) the structure of communication mandates under the CSDDD, which will align with the CSRD and subsequent European Sustainability Reporting Standards (ESRS), and 2) the adoption of a plan to transition to a sustainable economy through the obligations sets for CSDDD in-scope large companies on which the CSRD requires to report.

Both the CSRD and CSDDD reference the UN Guiding Principles on Business and Human Rights and the OECD Guidelines for Multinational Enterprises as foundational international frameworks for companies to conduct sustainability due diligence. Companies like IKEA, Siemens and Novo Nordisk have used them to start implementing comprehensive due diligence processes. These guidelines have a strong overlap with the CSDDD requirements and provide the following practical recommendations to support the implementation of sustainability due diligence processes:

1. Embedding the company’s approach to tackling adverse human rights and environmental impacts through policies and management systems

The first step is to formalize the company’s commitments and plans for implementing due diligence and start disseminating them throughout the organization and its business partners through policies and management systems.

2. Identifying and assessing risks

As a second step, a company will need to identify and assess areas of impact based on their severity and likelihood. Deeper evaluations of the issues will need to be undertaken once priority areas have been identified to better understand the company’s involvement.

3. Taking actions to address adverse impacts

If areas with potential risk are identified in step 2, it is important that a preventative action plan is developed with affected stakeholders, and where adverse impacts are identified, companies will need to minimize or even stop activity, depending on the issue and severity of impact.

4. Tracking implementation and results

Tracking the progress and effectiveness of the due diligence efforts can take various forms such as periodic internal reviews of the outcomes achieved and assessments of business relationships to verify that adverse impacts have been prevented or mitigated.

5. Communicating how impacts are addressed

External communication of relevant information on due diligence policies, processes and activities conducted to identify and address adverse impacts, including the findings and outcomes of those activities, is one of the last steps in the process.

6. Providing for or cooperating in remediation when appropriate

The last step is ensuring that remedies are provided to the affected individuals or communities (e.g., restitution or rehabilitation, financial or non-financial compensation, punitive sanctions) following relevant regulation and international guidelines on remediation.

The CSRD will inform the content of companies’ external communication under the CSDDD, while the latter, through the due diligence process, will inform the materiality assessments of companies as defined by the CSRD. Below are a few practical recommendations if your company is looking to make use of its SDD as part of its double materiality assessment:

• SDD will enable your company to identify stakeholders affected by your business activities and those of your value chain. Therefore, it is strongly recommended to use such inputs to form a comprehensive selection of stakeholders to be involved during your materiality assessment.

• SDD will also inform your materiality assessment by providing insights into the areas of significant impact that your business activities have on the environment and communities. These insights will also support the identification of sustainability risks and opportunities. So, when developing a list of potentially material matters, make sure to thoroughly consider the list of sustainability matters impacted by or likely to impact your organization, as identified through existing due diligence processes or enterprise risk management systems.

• Another way to make good use of SDD is through the impact materiality assessment process. If an impact prioritization procedure following the UN and OECD guidelines takes place within your SDD process, the severity and likelihood of your impacts have already been assessed and thresholds have already been set to determine priority impacts. These two elements can then be used as inputs into your impact materiality assessment. So, make sure to align the impact assessment approach used in your due diligence process (i.e., parameters for assessing impacts and threshold for determining priority impacts) with your impact materiality assessment.

With the foreseen entry into force of the CSDDD this year, companies are advised to start taking the necessary steps towards implementation of a robust sustainability due diligence process. Besides addressing negative impacts along the value chain, this is also an opportunity to reinforce their double materiality assessment under the CSRD.

Finch & Beak's vision is to create value beyond reporting. We support companies in preparing to comply with upcoming regulation, and moreover to get strategic insights out of your double materiality assessment, and leverage sustainability due diligence for ESG risk mitigation and gaining efficiency down the line.

If your organization requires practical support to get ready for CSRD and CSDDD, please contact us at hello@finchandbeak.com to discuss how Finch & Beak and SLR Consulting can support you.

Picture by Alex Gruber via Unsplash.

Finch & Beak

hello@finchandbeak.com

+34 627 788 170

Privacy Notice | Finch & Beak © 2024. All rights reserved.